Wall Street Sours On $9 Billion Mechanism For Green Projects

Yieldco shares largely haven’t recovered from turbulent 2015; Pension funds seek to acquire operating wind and solar farm.

Bloomberg

July 10, 2017

Wall Street investors have gone cold on one of the main mechanisms banks invented to fund the green-energy revolution.

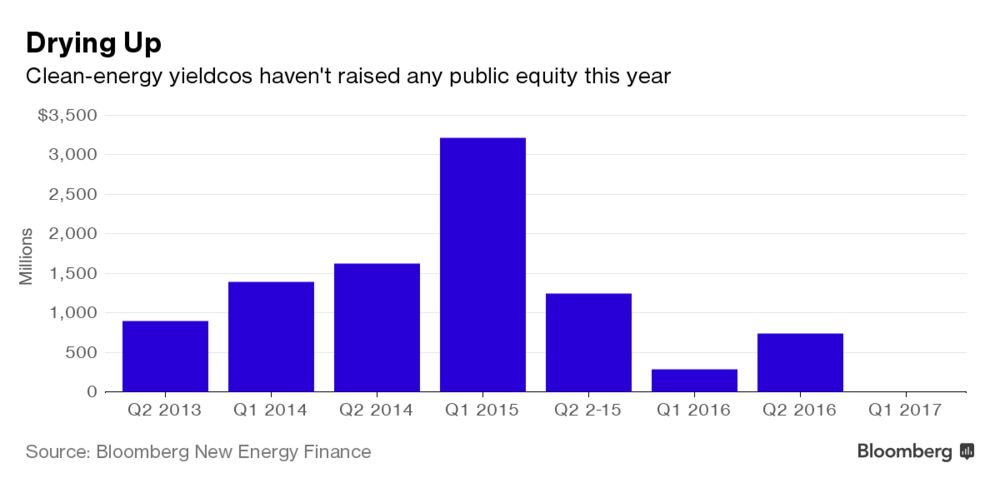

The business structure, known as the yieldco, feeds dividends from operating solar and wind farms to investors. Yieldcos raised $7.9 billion in public equity in 2014 and 2015 but only $1 billion since then, according to Bloomberg New Energy Finance.

The shift is further fallout from the collapse of yieldco promoter SunEdison Inc. and has changed the way clean-energy developers finance themselves. In years past, they started yieldcos to buy projects once they were operating, recycling the capital into new installations. Now, they’re turning to a large and deepening pool of buyers -- insurance companies and pension funds -- to provide funding and sometimes take control of income-producing assets.

“The idea of a you-have-to-have-a-virtuous circle -- that idea that you’re hooked at the hip between the public markets and growth -- is dead,” Mike Garland, chief executive officer of the San Francisco-based yieldco Pattern Energy Group Inc., said in an interview. “The market is saying, “‘Come to us last, not first.’ When we started, it was ‘Come to us first.”’

Wall Street investors have gone cold on one of the main mechanisms banks invented to fund the green-energy revolution.

The business structure, known as the yieldco, feeds dividends from operating solar and wind farms to investors. Yieldcos raised $7.9 billion in public equity in 2014 and 2015 but only $1 billion since then, according to Bloomberg New Energy Finance.

The shift is further fallout from the collapse of yieldco promoter SunEdison Inc. and has changed the way clean-energy developers finance themselves. In years past, they started yieldcos to buy projects once they were operating, recycling the capital into new installations. Now, they’re turning to a large and deepening pool of buyers -- insurance companies and pension funds -- to provide funding and sometimes take control of income-producing assets.

“The idea of a you-have-to-have-a-virtuous circle -- that idea that you’re hooked at the hip between the public markets and growth -- is dead,” Mike Garland, chief executive officer of the San Francisco-based yieldco Pattern Energy Group Inc., said in an interview. “The market is saying, “‘Come to us last, not first.’ When we started, it was ‘Come to us first.”’

Yieldcos first emerged in 2013, when the largest U.S. independent power producer, NRG Energy Inc., launched NRG Yield Inc. The parent formed the yieldco to hold operating wind and solar farms that it had built or acquired. Revenue from those assets funded dividends.

Pattern Energy and NRG Yield are projected to pay 12-month dividend yields of 6.4 percent and 6.5 percent respectively, according to data compiled by Bloomberg. That’s about three times higher than the average 2.1 percent yield of 500 companies on the Standard & Poor’s index.

The yieldco structure became a major growth engine for renewables, spawning at least eight yieldcos in North America and similar entities in the U.K. and continental Europe. Investors liked the story: support the growth of clean-energy while also reaping dividends that flow from electricity sales guaranteed by long-term contracts. And because the yieldcos promised to buy more and more projects, the dividends would only grow.

Fading Appeal

But headwinds -- most prominently the run-up to SunEdison’s bankruptcy in April 2016 -- stopped at least three other would-be yieldcos from forming and have forced others to eschew public markets for private fundraising. SunEdison had relied on its two yieldcos to finance its dizzying multi-continent buying-binge, thrusting them into turmoil and introducing doubt that the companies would be able to grow fast enough to pay rising dividends. The company’s struggles contributed to a broad renewables slump that made it more difficult to raise funds from the public equity markets.

As the business case for yieldcos has lost favor, a new group of buyer has emerged: pension funds and insurance companies hungry for wind and solar farms’ steady revenues. And the green bond market has boomed. Issues of bonds linked to environmental projects is set to surpass $100 billion this year more than 10 times the scale of the market in 2012, according to BNEF.

“The yieldco market got very heated,” Barry Gold, the New York-based head of Orix Infrastructure & Renewable Energy, said in an interview. “But we all know how things work in the financial markets: if a door closes, someone opens a window somewhere.”

Several yieldco owners see the writing on the wall. SunEdison, Abengoa SA and First Solar Inc. are trying to distance themselves from the units they created. Mark Widmar, First Solar’s chief executive officer, described the company’s 8Point3 Energy Partners LP yieldco as “a dormant vehicle basically.”

Pattern, meanwhile, is continuing as an owner of clean-energy projects -- the original intent of yieldcos -- but is now pushing into development. It recently bought a stake in an affiliated private company that feeds it projects, and it recruited Canada-based Public Sector Pension Investment Board to buy almost 10 percent of its stock.

“We’re short renewables in the U.S. -- and we want more,” Patrick Samson, a Montreal-based managing director at PSP Investments, said in an interview. “My pensions need long-term cash flows.”

Institutional investors are indeed emerging as a heavy of renewables M&A:

-- Alberta Investment Management Corp. in February agreed to buy one of the largest U.S. private solar companies, sPower, alongside AES Corp.

-- John Hancock Life Insurance Co. in March said it will buy a 49-percent stake in a clean-energy portfolio owned by Exelon Corp.

-- Activist investor Paul Singer may pressure NRG to sell its yieldco, potentially to capture institutional interest in wind and solar farms.

“Why not just sell to a pension fund?” said Jigar Shah, chief executive officer of clean-energy investor Generate Capital Inc. and a former SunEdison CEO. “There are literally hundreds of them that want these assets.”

Wind and solar farms typically have utility contracts that ensure consistent revenue streams, which neatly dovetail with the long-dated liabilities that insurers and pension fund managers accrue. For endowments, solar and wind investments help satisfy their heightened sustainable targets.

“The concept of pooling operational renewable-energy assets and selling to private investors will outlive the yieldco,” said Daniel Shurey, a New York-based analyst at BNEF, said by email. “The term ‘yieldco’ is going extinct.”

-- John Hancock Life Insurance Co. in March said it will buy a 49-percent stake in a clean-energy portfolio owned by Exelon Corp.

-- Activist investor Paul Singer may pressure NRG to sell its yieldco, potentially to capture institutional interest in wind and solar farms.

“Why not just sell to a pension fund?” said Jigar Shah, chief executive officer of clean-energy investor Generate Capital Inc. and a former SunEdison CEO. “There are literally hundreds of them that want these assets.”

Wind and solar farms typically have utility contracts that ensure consistent revenue streams, which neatly dovetail with the long-dated liabilities that insurers and pension fund managers accrue. For endowments, solar and wind investments help satisfy their heightened sustainable targets.

“The concept of pooling operational renewable-energy assets and selling to private investors will outlive the yieldco,” said Daniel Shurey, a New York-based analyst at BNEF, said by email. “The term ‘yieldco’ is going extinct.”

Article Link To Bloomberg:

0 Response to "Wall Street Sours On $9 Billion Mechanism For Green Projects"

Post a Comment